ESG Equals C.R.A.P.

This movement cannot die soon enough.

Here I will argue that the popular investment framework of ESG (Environmental, Social, and Governance) is flat out wrong. A better acronym would be CRAP (Contradictory, Risk-increasing, Amorphous, Political).

Attacking the ESG Components Head-on

It is a lot easier to be anti-DEI today. A bit harder is the position of anti-ESG. I choose the harder path because both are very bad in their own ways but importantly they are bad in a shared problem. They don’t work for the ends desired even when those are based on good intentions, and they have very bad byproduct downsides. I seek a complete end to the nonsense rather than a compromised outcome.

Let me take on the hardest cases as examples of each component.

Environmental:

I’m pro some pollution, and you are too. I am also in support of resource extraction to the point of capacity constraint. The reasons why is not an apology for things that are bad nor a defense of hypocrisy. Rather, it is an understanding that the world is filled with tradeoffs.

ESG seems to reject nuance. It also rejects the very basics of economic cost and the role they play in self limiting bad things. When I say we’re all “pro pollution,” what I mean is we know deep down that some level of pollution is not just tolerable. It is desirable. Zero pollution is impossible. Getting very close to it is undesirable because the costs exceed the benefits.

The most obvious cost is foregone benefits that are juice worth the squeeze. We know that automobile fatalities are at some level a cost we will allow for the benefits of driving—no reasonable person wants the speed limit universally set at 5 mph. Similarly, no reasonable person thinks we should all walk to work rather than drive in order to save the environment.

The less obvious cost is the unseen foregone benefits and actually higher levels of pollution extreme measures would entail. Walking to work wouldn’t just be tedious. It would make us poorer. Those benefits are huge, though, unseen. Even more unseen is the fact that when we are poorer, we have less resources with which to minimize pollution.

What about the dreaded gingivitis externalities . . . ESG is not a tool for internalization of negative externalities. It is a silly presumption that market-correcting policies are not possible so we need to act as investor advocates if we want them minimized. Now, I’m as big a critic of regulatory problems as the next guy, but the case for government regulation of market failures is theoretically sound. And there are success stories as well as good and better ways of doing it. Pigouvian taxes, cap-and-trade, traditional government regulation like the EPA, tort law, etc. are all ignored by ESG as nonexistent or unworkable.

Social:

I’m pro “sweatshops” and even child labor. [HORROR!] But I am firmly against slave labor. [phew]

Paul Krugman was right we he wrote in defense of “sweatshops” nearly 30 years ago. I like this extreme aspect of the issue because it most starkly calls out the problems with ESG—that it enables bad policies in the name of good intentions.

As Krugman pointed out, the unfortunate tradeoff for those in poor economies is a bad versus less bad options. The tradeoff is never very good things versus bad things. This is the state of nature that humans have struggled against for all time. If we compare working conditions between a given economy today and that same economy in the past, we see a world we would not want to return to. Future generations will look back with sad sympathy if not horror at conditions (working and otherwise) that exist today—we don’t know how bad we have it now in comparison to our likely future if we can maintain even a modest level of economic growth.

Similarly, when we compare working conditions in poor countries today to those in rich countries, we find uncomfortable differences that any kind person would rightfully recoil at. But while it is emotionally tempting to reach for easy solutions to this dilemma (“there should be a law!”), rational minds realize it’s not that easy. The realistic solution is let economic growth do its thing while maintaining and striving for truly free markets—especially freedom for workers. This is not in any way a condoning of coercion.

We would like to think getting rid of the bad working conditions (including child labor) would make the world better for those we rightfully are being sympathetic to. But reducing people’s options including importantly taking away their first best (least bad) among altogether bad options does not make them better off.

Governance:

Racial and sex diversity is virtue-signaling intention without substance (social-desirability bias) at best and bigotry masquerading as a new, beneficial idea without a downside at worst. Thought diversity is what matters—diversity both in methodology and goals. You cannot measure on-going bigotry (pro-white, pro-male, etc.) by looking at the racial or sex composition of a group—especially a small group. It undoubtedly and sadly existed, certainly continues in some form today, likely lingers in outcomes despite where it is explicitly legally extinguished, and yet cannot be overcome by simply manipulating the superficial makeup of the people in the room.

CRAP Defined

Contradictory - Each of the examples above show ways in which ESG works at cross purposes to its alleged goals. There are many more such as favoring what sounds good over what is good from the perspective of an ESG goal itself. I expand upon this in the amorphous section below.

But there is another version of the contradictory nature of ESG. It drains resources from investors with benevolent hearts by lowering their expected return and diminishing their voice. As I’ll expand upon in the political section, sitting outside of the boardroom or with no vote on the proxy is no way to affect change.

From the lowered return point of view, IF it were the case that there were gains to be had from using an ESG framework in investing, then we’ve discovered a free lunch. Alas, TANSTAAFL strikes again. In reality the ESG theory implies that the boycotted investments will go down in price, which will raise their implied expected return. Investors who then participate with these naughty investments will be the beneficiaries leaving the ESG investor holding an inferior portfolio.

Risk-increasing - I imagine it would surprise proponents of ESG, but theory and practice tells us that following an ESG guidance in which our investment options are limited will increase the risk for any given expected return. The reason why is straightforward: The ESG limitations are reducing diversification if they are meaningfully implemented.

One of the best examples of this is the energy sector where over 80% of it is in fossil fuels. While ESG apologists will insist that many of those companies are compliant (to some degree), the more that is true the less truth there must be in the complaint that fossil fuels, et al. are an issue for ESG to address. At some point being ESG compliant must simply be window dressing. You can’t have it both ways.

This problem of excluding most of an important sector is just the tip of the (melting) iceberg of how ESG rules will lead to “good” sector concentrations due to exclusions of “bad” companies and industries. The harder it is pushed the bigger the increase to risk from less diversification.

NYU professor Aswath Damodaran is among many great sources for the problems with ESG, which he labels “an empty acronym, born in sanctimony, nurtured in hypocrisy and sold with sophistry.” He has a lot to say about the problems with ESG, not the least of which is how it increases risk (see slide 9 of this presentation).

Amorphous - ESG suffers from the motte-and-bailey fallacy. Whenever challenged, proponents retreat to the most modest and unarguable claims, which amount to nothing but banality. These bromides are of course true and shared by all and tell us nothing.

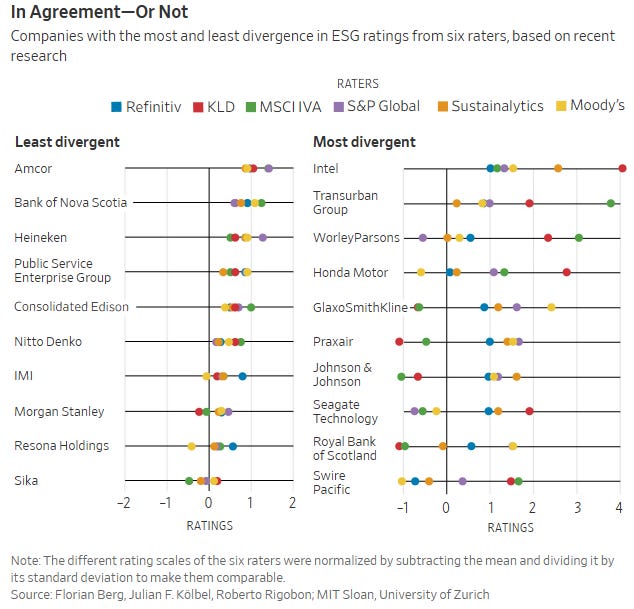

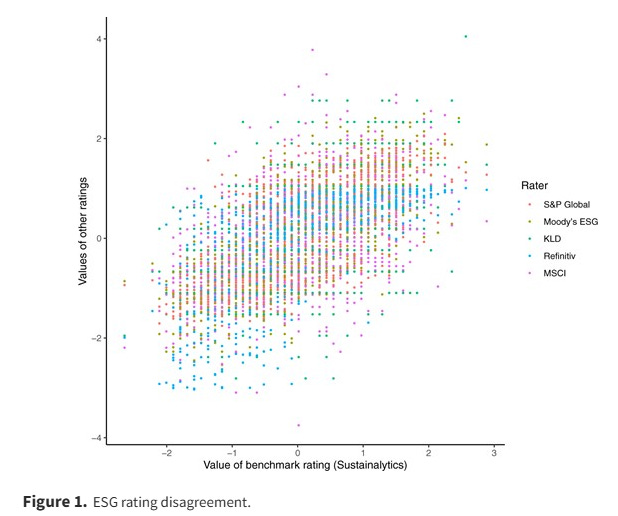

The amorphous problem with ESG can be seen most clearly in how difficult it is to define what an ESG-compliant investment actually is. One way to see this problem was explored in a paper by researchers at the MIT Sloan School of Management. Among other findings, they examined how differently the same companies were rated by various ESG scoring firms. The first chart below is from a WSJ article done by one of the authors, Florian Berg. The other is from the paper itself.

It seems being ESG compliant is in the eye of the beholder. That suggests deep problems with the thesis. Digging deeper than these charts, the authors found many indications of bias in the rating results.

There are a couple more amorphous problems with defining who is naughty and who is nice. For one, our values change. Are gun manufactures good? What about when we consider the need for self defense? The issues of the day from the summer of 2020 (police brutality or rioter risk) to the ICE protests of today and other issues like freedom movements in dictatorships make this a shifting sand. How about pharmaceutical firms? Are vaccines good or bad? What about abortifacients versus life-saving drugs made by the same firms? Again, ESG can be in the eye of the beholder. While I strongly support people’s individual desire to express their political, social, and moral views, that individualized process or outcome are not what ESG was sold as.

For another, ESG seems to look the other way when its implications become untenable. Selling WMDs is bad but owning much less using them is good? To be consistent, any ESG exclusion for weapons manufacturers should also consider excluding U.S. government bonds. Good luck getting that past the investment committee. These inconsistencies speak to why for many the “S” in ESG seemingly stands for Sometimes.

A central question emerges from all of this: Are you substituting what sounds good for what is actually good? If ESG cannot define bad and good properly, it fails at its primary task before any of the other issues are even considered.

Political - For a fiduciary, there is little to no place in investing for politically-based decisions. Related to the risk-enhancing nature of ESG, forcing the additional constraint on a portfolio that it cannot invest in certain out-of-favor investments always must come at a cost. The fools and liars behind ESG sold this constraint as a return-enhancing virtue when there was no reason to believe it could be. And as it relates to the amorphous problem, this constraint either binds the investor from making optimal decisions or simply restates at the risk of over-indexing that which they should already be doing.

Companies or bond-issuing governments who have poor earnings or governance qualities including bad policies regarding risk (pollution, socially-destructive products, etc.) already compensate investors with higher expected returns. To exclude them is to exclude accretive opportunities. If these are not properly priced in, then they already fail the investment test before the ESG oversight. To claim ESG is bringing this to our attention as investors is a slight of hand.

Investment decisions based upon moral choices is a cost. There is a tradeoff to be calculated. Often investors are willing to make this bargain, but they need to understand it is something they are giving up (expected return for moral high ground)—not a win-win. And this tradeoff should include the bigger picture. An investor does have a voice. They can influence corporate or governmental policy as a stock or bond holder. But importantly their boycott will almost certainly not change the problematic firm or government’s cost of capital. And if it does, it simply increases the expected returns to those investors willing to make the investment—those who presumably do not care about the offending practices.

Conclusion

It is always prudent to take a skeptical eye to the latest investing fad. With ESG I think being an outright cynic is appropriate. ESG is a tool by Wall Street to earn larger fees by selling good feelings and false promises to well-intentioned investors. It is a classic bootleggers-and-Baptist story.

ESG may very well have started as an effort to enhance investor analysis. After all, these are all important considerations in making investments—at least in theory and proper dose. But they weren’t new. Astute investors have always considered the environmental, social, and governance aspects of an investment and the underlying firm or government. ESG amplified this component of investment analysis to an unhealthy degree—unhealthy for investors and society, but very health for the investment firms selling this charade.