Economics is not so much hard to understand as it is hard (for many) to accept. I’ve found in years of conversation and at various times formally teaching that people’s instincts are pretty good with just a little coaxing and guidance. Yes, much of economics can be counter-intuitive. But I think this is largely because our intuitions are polluted by emotional desires and bad actors who play on those emotions.

Let’s start down this path with a video.

In this interview by John Stossel, Don Boudreaux succinctly explains the case for economic freedom. It is a very accessible explainer inviting those interested to learn even more from Boudreaux's recent book with Phil Gramm, The Triumph of Economic Freedom. Send this video to those in your life confused by the current economic-political landscape.

Now let’s go a little deeper touching on something that shallow critics of economics love to latch on to—the idea that economics rests on a bad assumption of a rational actor.

Josh Hendrickson demonstrates in his post “Panhandlers and Price Theory” that this is a mistaken accusation. Using panhandling and dovetailing off of his other recent posts on drug use he provides a great example of why price theory does not rely on the critic’s strawman version of rational actor. Rationality emerges from even “irrational” people. Chicago market economics for the win!

I also like examining topics like this precisely because they highlight what price theory is and is not. Price theory is a framework for understanding, explaining, and predicting human behavior. Price theory is not a theory of mind.

. . .

Suppose that you wanted to test this idea that, all else equal, competition tends to equalize rates of return on particular types of investments or activities. How could you do it?

. . .

For example, think of a situation in which there is (a) free entry, but (b) some reason to believe that the competitive model might not apply. If one finds evidence in favor of the competitive model under those conditions, then that is pretty strong evidence in support of the model.

One such example is that of panhandlers. It seems pretty clear that there are places in which panhandling is perfectly legal and there is no restriction on panhandling. The absence of those restrictions suggests that anyone can show up and panhandle. As a result, if panhandling turns out to be quite lucrative, we would expect to see people switch to panhandling from some alternative use of their time. In fact, competition in panhandling should drive down the rate of return on panhandling until it reaches the opportunity cost of the marginal panhandler.

. . .

Setting aside whether competition equalizes rates of return across different stations, one simple test would be to see if panhandlers follow basic economics incentives. For example, one would expect that there would be more panhandlers at the busier stations and the friendlier stations. One would also expect that there would be more panhandlers where the barriers to entry are low, such as at stations where there is a shuttle stop for the homeless nearby.

This is precisely what [researchers Peter Leeson, August Hardy, and Paola Suarez in their recent paper] find for the full sample.

He concludes:

Critics of economics generally, and price theory in particular, tend to argue that we assume that everyone is a hyper-maximizer, only concerned with self-interest and that the world is more complicated than that. People aren’t walking around all day solving utility- and profit-maximizing problems in their head. Not everyone is a rational calculator.

I think that we can reject these criticisms. I am not saying that we should reject them on the grounds that they are false characterizations of the real world, but rather that they are a false characterization of price theory. As I wrote in my previous posts, price theory is about providing rational frameworks to understand, explain, and predict human behavior. It is about rational frameworks, not rational people.

Going deeper still I share two from Scott Sumner. In the first post he explores the usefulness of tautologies examining six.

I don’t know how many times I’ve heard the news media attribute a sharply decline in stock market indices to a “selling wave” hitting Wall Street: The Dow fell 800 points as investors sold 15.4 billion shares of stock. Yes, but investors also purchased 15.4 billion shares of stock.

At one time, the stock market was closed at night and yet market indices often changed dramatically, even without a single share being traded. A hundred years ago, the Dow might close one day at 243 and open the following morning at 227, reflecting bearish overnight news. In that case, it is fairly obvious that the market moves on new information, not trading activity. To the extent that trading activity has any impact on prices, it is due to what the trading reveals about information held by various participants in the market.

In these examinations of tautologies he highlights wisdom that can be obtained from understanding them including organizing our thinking to see causal connections. This includes rejecting bad reasoning such as reasoning from a price change.

I’ll give two slices. The first is using the tautology that savings = investment:

Unfortunately, many people misinterpreted Keynes’s “paradox of thrift” as a claim that more saving is bad for the economy. That’s not what Keynes said!Keynes argued that a decline in aggregate demand (basically nominal spending or NGDP) is bad for the economy, and that this sort of decline might be caused by an increase in the public’s desire to save. But Keynes never said that more saving is itself a bad thing, as he understood that in equilibrium there is an equality between saving and investment. And since Keynes was very much pro-investment, that means he was also very much pro-saving.

The second is using the tautology that aggregate supply = aggregate demand coupled with Say’s Law:

Here’s AI Overview:

Say’s Law, often summarized as “supply creates its own demand,” posits that the production of goods generates the necessary income (wages, rent, profit) to purchase that total output. It implies that general overproduction or widespread “gluts” are impossible in a market economy, as total demand always equals total supply.

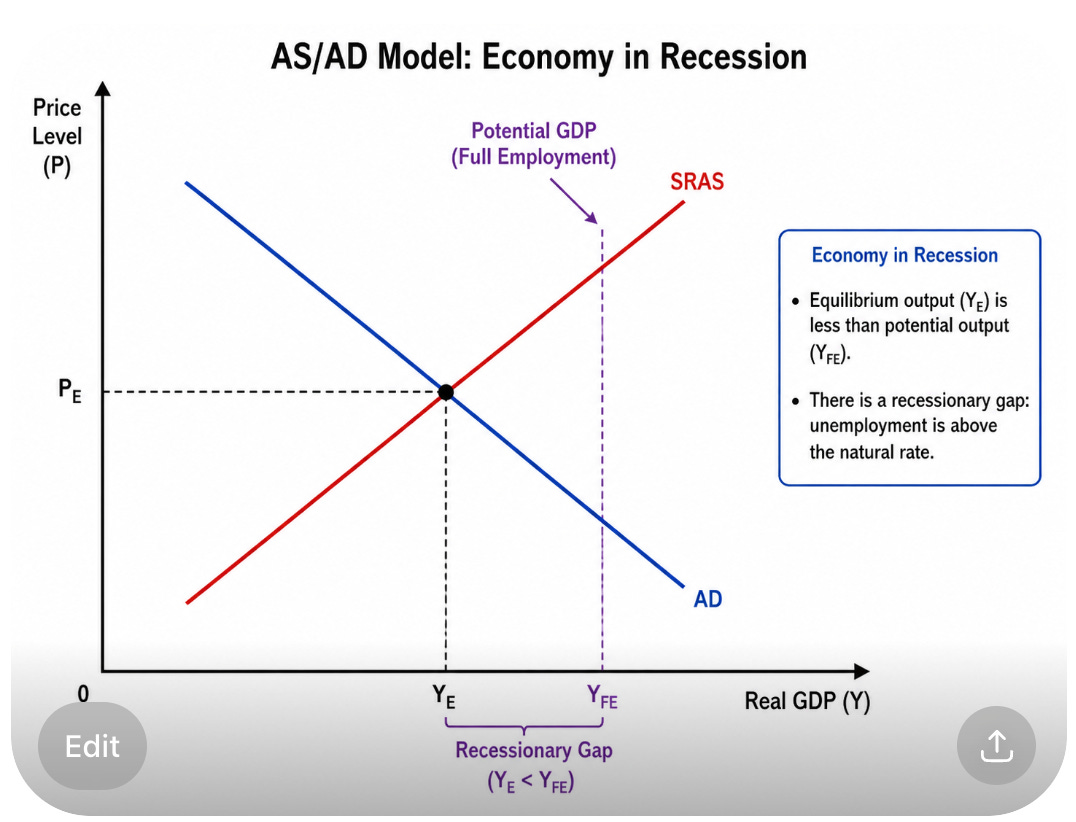

When defined this way, Say’s Law is true. The Great Depression was not caused by overproduction (as Franklin Roosevelt believed), rather it was a case of too little production. On the other hand, Say’s Law does not mean that we need not fear a situation where nominal spending is falling. Even if aggregate supply equals aggregate demand in a Depression, the equilibrium may occur at a undesirably low level of output and employment:

[Graph courtesy of ChatGPT]

Much of the confusion is due to the use of the term “aggregate demand”. I wish the model were called the nominal spending/real output model, not the AS/AD model. It has nothing to do with “demand” in the ordinary sense of the term as used in microeconomics.

The second post from Sumner is his take on the Committee for a Responsible Federal Budget’s (CRFB) plan to save Social Security, which he both praises and laments as politically implausible.

In praising and explaining the implications of the CRFB's proposal, Sumner effectively works the body on two separate fronts. He makes the case that the reform is essentially a progressive consumption tax with the economic and fairness benefits that policy change would imply while also demonstrating wealth and charity aren't well understood by the common man.

Starting with the tax part:

The CRFB’s proposal is essentially a progressive consumption tax, although it won’t look like that to the average person. I cannot teach an entire course in public finance theory in a blog post, but the essence of a consumption tax is as follows:

Imagine a world where people can either spend $6000/month on consumption today, or $12,000/month on consumption in 20 years, by saving their incomes. Now assume you impose a 33.3% tax in that world, which takes away a third of the public’s resources for consumption. With a pure consumption tax, your choice is now $4000/consumption today or $8000 consumption in 20 years.

Notice that the “terms of trade” have not changed, in both cases, the opportunity cost of a dollar spent on consumption today is foregoing two dollar’s consumption in 20 years. A consumption tax is a tax that does not change the relative price of current and future consumption. In a sense, all taxes are consumption taxes, as the burden of any tax is its impact on a person’s lifetime consumption. However, economists use the term “consumption tax” to refer specifically to taxes that treat current and future consumption equally. An income tax punishes savers and hence is not a consumption tax.

I’m pretty sure that most people don’t understand this concept, as I often see commenters say things like “we should tax consumption, not labor.” Actually, a labor tax is a consumption tax. Indeed, these three taxes are all equivalent consumption taxes, in the long run:

1. A 20% VAT

2. A 20% payroll tax on wages

3. A 20% income tax with unlimited ability to put savings into a 401k plan, and no mandatory date of withdrawal from the 401k. (Funds borrowed for consumption are also taxed.)

Note: Although I think I usually say something like “we would tax consumption rather than capital,” I’m sure I’ve made the sloppy mistake he points out of saying “we should tax consumption rather than labor.”

After fully describing how the CRFB’s plan is desirable, he turns to the implausibility basing his case on how people misunderstand wealth and charity.

Unfortunately, the CRFB plan seems too good to be true, and I expect Congress to implement something far worse. In order to understand why, consider two neighbors that both spent their careers in upper-middle class jobs making close to the Social Security taxable maximum (currently $184,500). Both retire as single people entitled to roughly $50,000/year in benefits. Both would see their benefits capped in nominal terms, which means their real benefit levels would decline over time.

But these two neighbors differ in one very important way. Smith was a high spender who would buy the latest BMW, while Jones was a high saver who always bought used cars. Smith saved very little while Jones maxed out his 401k plan.

Now Smith starts whining to his congressman that the proposed cap is unfair. It should only apply to “the wealthy”. His neighbor Jones is now pulling $100,000/year out of his 401k and doesn’t “need” his Social Security benefit to rise with inflation. “Please make the cuts depend on income levels, not benefit levels.” Because America has far more grasshoppers than ants, Congress listens to the whiners and applies benefit cuts only to those with high current incomes, not those with high lifetime wage incomes. They punish savers and reward spendthrifts.

. . .

People focus on the fact that those who are currently wealthy have more resources than the less wealthy, even when the gap is 100% due to the less thrifty person choosing to spend at an earlier stage of their lives. In my thought experiment, the two neighbors were equally wealthy in the only way that matters—they had equal lifetime resources to allocate to consumption and simply choose to do so at different points in time. Smith consumed when he was young enough to enjoy it, and Jones foolishly waited until he was old, wrongly imagining that he could still get a thrill out of life at age 70.

. . .

There’s an ongoing debate over how much money billionaires ought to donate to charity. Unfortunately, most people miss the point. The issue isn’t charity vs. investment; it is consumption vs. non-consumption. A charitable person is an individual that doesn’t consume much relative to his or her wealth. If you wish to consider heirs, you might say a charitable person is someone who ensures that he or she and all their future heirs consume only a modest portion of their current wealth.

But you can also argue that a charitable person is someone that maximizes their wealth, given the share of that wealth that they intend to use for consumption (both they and their heirs.) A wealthy person can become more charitable by reducing long run family consumption of wealth from 40% to 30%, but also by increasing their total stock of wealth and keeping the consumption share at 40%.

. . .

As Matt Yglesias recently pointed out, those billionaires that consume a large share of their wealth are the actual problem.

. . .

To be altruistic is to forego consumption for you and your heirs. That’s it.

[emphasis in the original in all cases above]

He ends with two great quotes. One is favorite of mine from Steven Landsburg that I have referenced before about misers being the ultimate philanthropists. The other is Bastiat's greatest insight, “That which is seen, and that which is not seen.” Another from Bastiat came to my mind while reading the post: “The State is the great fiction by which everyone seeks to live at the expense of everyone else.”

P.S. As if right on cue, Landsburg brings in another with this post making the same essential point about people confusing money transfers with wealth transfer:

I doubt very much that Mr. Musk plans to spend a trillion dollars before he dies. Suppose instead that he plans to spend, say, a hundred million. Now suppose he gives away all his money (or we confiscate it) and he reduces his lifetime consumption to zero. That leaves an extra hundred million dollars worth of food, clothing and fuel for the rest of us. Divide a hundred million dollars among three hundred and fifty million Americans and you get not $2800 per person, but 28 cents. That’s how much extra stuff the average American can now buy.

Whatever Elon gives to John, Paul and George must ultimately come from Elon. What’s available to others is capped by what he sacrifices. In fact if you confiscated, say, half of Elon’s wealth and he chose to go right on consuming at the same rate, then the total value of what you could redistribute would be exactly zero.

What if you ignore all that, take Mr. Musk’s trillion dollars and redistribute it anyway? Or what if Elon himself ignores all that and decides to give a bunch of money away? The answer, in either case:: We all get $2800 checks, we all feel richer, we collectively try to buy an extra trillion dollars’ worth of stuff, there’s only an extra hundred million dollars’ worth available, so prices and/or interest rates adjust to the point where your $2800 check can purchase only about 28 cents worth of goodies.

Magnitude Matters is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.