My objectives today are straightforward. I want you to learn three things. You will have the ability to get the high-level, so-called “30,000-foot-view”, or the full monty.

We need to Stop Banning Housing, where the latest and last possible iteration of this is the movement to ban corporate investments in the rental market.

We need to relearn the story of the Great Recession, which includes there wasn’t a housing bubble, subprime problems were a minor character in the play, the banking crisis came from the recession rather than being a cause of it, and the solution wasn’t to scale back but rather to ramp up production to escape the economic problem.

We need to dismiss the assertions of Thomas Piketty that inequality in capitalist countries has been growing worse and will continue to worsen because, so goes the argument, the return to “capital” exceeds the return to the rest of the economy.

If you wish, stop there. You won’t really know these counter arguments, but at least you’ll stop thinking much less repeating foolish stories. And perhaps you’ll be able to inoculate yourself against the tide of just-so stories and wishful thinking that underpins these myths.

If you’re like me, you’d like to go deeper. So let’s.

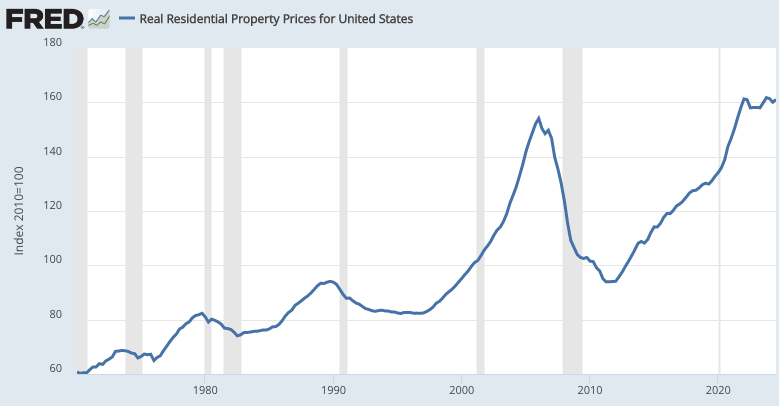

In the first case Kevin Erdmann in a short video breaks down where we are in the housing market (a 70-year decline in housing investment culminating in a flatlining since the great recession), how we got here and why people misinterpret the situation (mistaking inadequate supply with runaway demand—reasoning from a price change), and why worries about corporate investment are so misguided (it is the last hope for building housing for American families).

There is a lot more in the video including very helpful graphs and analysis.

Hand in glove with this is the second case where Scott Sumner works through 18 misconceptions, Macro Myths, regarding the Great Recession.

I absolutely love this post. Obviously, I love counter conventional wisdom thinking, but I especially love it about a topic as important and misunderstood as the Great Recession.

Of his 18 myths, it is hard to pick a favorite. Here are a few that stand out:

There was a housing bubble that peaked in early 2006.The term ‘bubble’ often refers to excessive rates of new home building and/or irrationally inflated home prices. The US was not building too many homes in 2005-06; if we were you’d expect falling house prices, not rising prices. Indeed the inadequate level of home building during recent decades (due to the excesses of Nimbyism) is arguably the biggest economic problem in America. It is one of the most important reasons that living standards for the middle class have been rising more slowly than during the mid-20th century. In addition, there is no evidence that housing prices were irrationally high during the 2005-06 boom. If high housing prices caused the Great Recession, why didn’t the equally high (real) housing prices of 2022 cause a recession? The high housing prices of recent years are fully justified by the “fundamentals”.

The subprime mortgage fiasco largely explains the banking crisis.Most of the bank failures during the Great Recession occurred because of defaults on commercial loans, not subprime mortgages. This is exactly what you’d expect to occur when there is an unusually dramatic decline in NGDP growth. The banking crisis is not a puzzle that needs to be explained; the puzzle would be if an 8% drop in NGDP growth rates did not cause a banking crisis.

The banking crisis caused the Great Recession.The post-Lehman banking crisis occurred 9 months after the recession began, just as the banking crises of the 1930s occurred well after the Great Depression began. Again, banking crises are a symptom of falling NGDP, not a cause. Think of nominal GDP as the income that people and business have available to repay nominal debt.

After the debt crisis, it was appropriate for aggregate demand to decline. Americans needed to “tighten their belts.”This conflates aggregate demand with consumption. When you’ve gone too far in debt, it makes sense to work harder, not take a long vacation. For a country, the response to too much debt should be more employment, more work effort, more production, not less. That’s how you “sacrifice”.

The Fed did all it could to boost the economy in 2008; it simply ran out of ammunition. There are two problems with this claim. The Fed didn’t even cut its target interest rate to a level close to zero (actually 0.25%) until mid-December 2008, by which time most of the decline in NGDP had already occurred. In addition, the Fed has many tools that it can use after interest rates hit zero. Fiat money central banks never “run out of ammunition.”

Last is Michael Mungerthrowing cold water on the incendiary arguments of Thomas Piketty.

This is a long post. I encourage ambitious readers to read it in full. I invite everyone to at least skim it. It is a master class in explaining and taking down the many doomsday and anti-capitalist claims of economist Thomas Piketty.

From his conclusion:

Piketty’s argument consists of two parts: an empirical claim (vast increases in inequality) and a theoretical explanation (capital has a higher return than labor). Each of the two components has crippling flaws, so the Piketty model fails, on its own terms. There are four reasons for this failure:

1. “Capital” is not homogenous.…

2. Even if capital were (more) homogenous, the depreciation of capital is not fully offset by increased saving by the wealthy.…

3. Nearly half of what Piketty calls capital is tied up in the value of dwellings, and the land on which dwellings are placed.…

4. Finally, wealth held as real estate, or other physical forms of capital structure, are complements to labor, not substitute.…

Thus, while Piketty’s work has been heavily employed as a focus of inequality and “social justice” research, Piketty’s conclusions are mostly misguided. Any policy responses based on them will be, too. Inequality and poverty are significant problems, and the sense of precariousness felt by many Americans is real. Unfortunately, the exaggerations and excessively pessimistic claims made by Piketty and those whom he has persuaded to follow his arguments have likely made the problems harder, not easier, to solve.

When the popular narrative becomes corrupted, it is very likely to become the prevailing wisdom. As such, it gets into the school-house curriculums and history books as well as in the ears of politicians from the lips of voters. From there it continues to do damage as we fail to learn from the past—allowing repeated failures.

Magnitude Matters is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.