During the 19th century, the US had roughly zero inflation, on average, despite some fairly high tariffs. Indeed the “cost of living” in 1933 was still about the same as when the country was founded in 1776. Does this surprise you? It shouldn’t. In this post I’ll explain why the Trump tariffs are not likely to be very inflationary, but nonetheless will be bad for the economy.

Consider the following two claims:

Claim #1:

In 1925, a quarter could purchase about 5 quarts of gasoline.

Today, a quarter can purchase barely a cup of gasoline (at $4.16/gallon).

Claim #2:

In 1925, a quarter could purchase about 5 quarts of gasoline.

Today, that same quarter can still purchase about 5 quarts of gasoline.

Both claims are true, at least here in California. Back in 1925, gasoline cost about 20 cents per gallon. So a quarter could buy about 5 quarts of gas.

The 1925 quarter contains 0.18 troy ounces of silver. So when silver is selling for $30/oz., the old quarter contains $5.40 worth of silver. This means a 1925 quarter can purchase still roughly five quarts of gasoline (assuming the current dollar price of gas is $4.32.)

You might think that both silver and gasoline have become much more valuable since 1925. But that’s just a cognitive illusion, or perhaps you could call it the money illusion. In reality, it is fiat money that has become much less valuable.

Today, we are so used to a persistently rising cost of living that people are surprised to hear about the relative lack of inflation prior to 1933. They are surprised that persistent inflation only applies to post-1964 (copper/nickel) quarters, not pre-1964 (silver) quarters. And yet there’s nothing unusual about the old quarters, it’s the new ones that are weird.

Nominal price changes reflect a change in the value of one asset (gasoline) in terms of another (money). Ex ante, it’s not obvious why you’d expect the value of any given asset to rise or fall over time. It would depend on the supply and demand dynamics in the market for silver and for gasoline. That’s why with commodity money standards (usually silver or gold), the average rate of inflation was roughly zero, although there can be short-term volatility, as with the relative price of any two commodities.

Thus it is the recent persistent inflation that is odd, not the ups and downs of prices from 1776 to 1933. The cost of living rose somewhat after we devalued gold in 1933, but really took off when we removed silver from money in 1964 and stopped pegging gold at $35/oz. in 1968.

But even paper (fiat) money is not necessarily inflationary. It has turned out to be inflationary in the US, but fiat money in Japan and Switzerland has not been particularly inflationary during recent decades. It depends on monetary policy:

It is a great post that touches on several other points.

Protectionist: Over the past half-century, American industry has been hollowed out by international trade. We don’t make things anymore. That’s why we need protective tariffs.

Boudreaux: You’re factually incorrect. US industrial output hit its all-time peak in February of this year, higher by 155 percent than it was in 1975, when America last ran an annual trade surplus and 19 percent higher than in 2001, when China joined the WTO. Also, US industrial capacity is at an all-time high, and 147 larger than in 1975 and 12 percent larger than in 2001. Tariffs only —

Protectionist: Sorry for interrupting, but I don’t believe those government statistics. Bureaucrats are politically biased, with no incentive to get things right.

Boudreaux: Do you hear yourself? You don’t trust government officials to competently gather and report economic statistics, yet you do trust government officials with the power to coercively obstruct your and other Americans’ peaceful commerce with foreigners. How does that make sense?

Protectionist: I know what I see. Boarded-up factories, ruined lives, nothing made in America. You’re telling me that my own eyes are lyin’. I’m telling you that I believe my eyes and not free-traders’ lies, damn lies, and statistics.

Boudreaux: How many boarded-up factories do you actually see — in reality, not in photos — on a regular basis? If what we literally see with our eyes is the only guide to reality, then my eyes, seeing not a single shuttered factory, tells me that no such things exist. Whose eyes should be believed? Even if you happen regularly to encounter such sights, these aren’t the norm in the US. We need statistics to get an accurate picture of the economy.

Now it’s true that statistics can mislead, but they can also reveal and enlighten. It’s foolish to leap from the fact that statistics are sometimes used deceptively or carelessly to the conclusion that all statistics are unreliable. Indeed, you yourself rely on statistics whenever you assert, as you often do, that nineteenth-century US economic growth was fueled by tariffs. After all, your eyes weren’t around in the 1800s to do any observing. Your argument depends on you knowing that, in that era, US tariffs were often high and America’s economy grew at a rapid pace — both bits of knowledge being statistical.

Protectionist: Look, all I know is that America had high tariffs in the high-growth nineteenth century. Hard to argue with that!

Boudreaux: Actually, even beyond pointing out that you commit the sophomoric error of mistaking correlation for causation, it’s quite easy to argue with your assertion. Phil Gramm and I, in our new book The Triumph of Economic Freedom, look at annual growth rates of US industrial production in the nineteenth century. We find that industrial output grew faster in periods when tariff rates were falling than in periods when tariff rates were rising.

But beyond this fact, America back then was economically quite free, very entrepreneurial, and so large that most economic activity was purely domestic. International trade played a relatively minor role in nineteenth-century US economic growth. A greater role was played by immigration.According to the economic historian Robert Higgs, the US in the latter half of the nineteenth century experienced “the greatest volume of immigration in recorded history.”

If you conclude that the co-existence in nineteenth-century America of protective tariffs and rapid economic growth proves that protective tariffs fuel economic growth, then you logically must also conclude that the co-existence in nineteenth-century America of enormous immigration and rapid economic growth proves that enormous immigration fuels economic growth. Should we return today to the immigration policy that reigned in the US in, say 1870, when our borders were almost completely open?

Protectionist: Let’s stick to tariffs, shall we? When I go to Walmart and Target, or buy stuff on Amazon, all the labels read “Made in Vietnam,” “Made in Bulgaria,” “Made in Mexico” — never “Made in America.” Nothing today is made in America. My eyes don’t deceive me.

Boudreaux: No, but your limited knowledge does. Those labels don’t mean what you think. In today’s global economy, the great majority of the manufactured goods that you consume consist of parts and ideas from around the world, including the US. A “Made in” label on some good tells you only where that good’s final assembly occurred. Bath towels at Target labeled “Made in Turkey” might well be made of cotton grown in Texas, dyed with pigments from Germany, woven on a loom made in India, and shipped to the US on a freighter made in Korea that is carrying a shipping container manufactured in Denmark. That label would be more accurate if it instead read “Final Processing Done in Turkey” — or, more accurate still, “Made on Earth.”

Because the final processing of most consumer goods is a relatively low-value-added task, Americans’ high wages make it worthwhile for manufacturers to have those tasks performed by lower-wage non-Americans. But goods labeled “Made in Turkey” or “Made in China” frequently contain more inputs made in the USA than in the country named on the label.

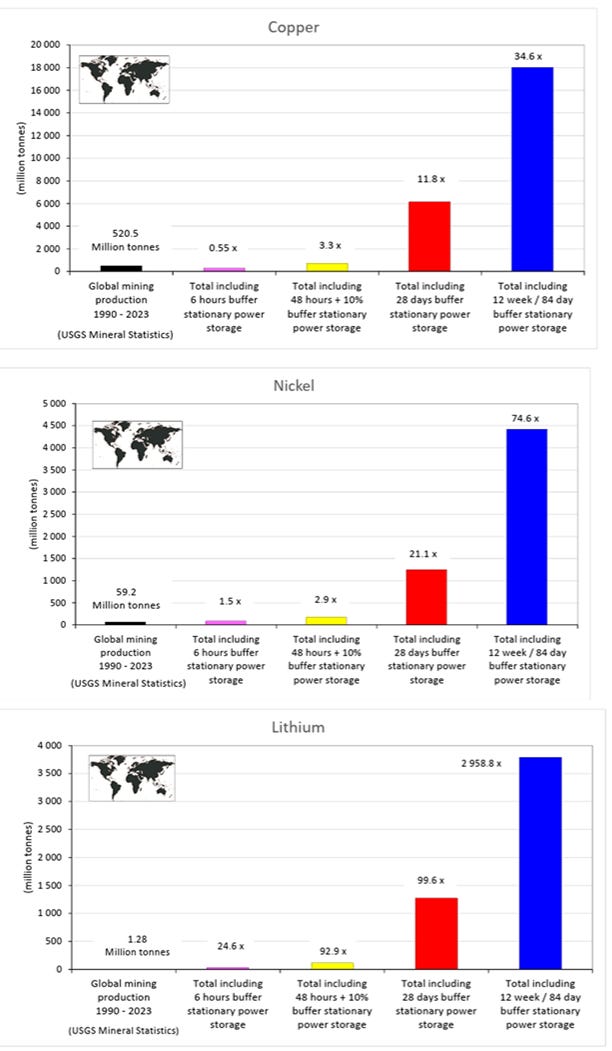

~700 million tonnes of copper are implied by a net zero pathway over the next 22 years. That is equal to all of the copper ever mined over human history. Source: Geological Society of Finland.

…

The image below shows the implied metals requirements for copper, nickel, and lithium, under different assumptions (the study discusses many more metals). In each panel the short black bar on the left shows total global mining production for 1990 to 2023. The bars to the right of the black bar show the metal requirements implied by different amounts of battery storage in a net zero energy system. Of the large blue bar on the right, representing 84 days of storage, the study says it “may well be still too small” to adequately buffer delivery of electricity.

…

Bottom line: Always do the math — You might be surprised what you learn about what was previously assumed.

In these three posts we have Sumner demonstrating how inflation is a nuanced concept, Boudreaux showing how easily confused most people are when it comes to trade, and Pielke revealing the colossal (near-impossible) implications of achieving a net-zero fossil fuel future any time soon. Do read all three in full. There is a lot more there than the excerpts I selected.

Magnitude Matters is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.