The Future Landscape for Real Estate

Land, are you sure "they ain't making any more of it"?

I think many things tend to move in cycles that are just long enough for them to be too long for us to perceive them as cyclical rather than never-ending trends. Herb Stein’s law is important here—if something cannot go on forever, it will [eventually] stop. But equally important is the wisdom of philosopher Bon Jovi.

Sometimes the cycles don’t have to be long to be long enough such as when a football team just keeps winning at an extraordinary rate. Alabama comes to mind here with their tremendous success under Nick Saban. Since he took over as head coach for the Crimson Tide in 2007, the team has won almost 88% of its games through 2021 (a 178-25 record). But in the preceding 15 years the team only won 51% (a pedestrian 84-80 record).

Sometimes the cycles are quite long indeed. Regardless of your views on climate change, the fact is the climate does change meaningfully over long periods of time—decades, centuries, and millennia depending on the type of change being examined.

A system subject to cyclical phenomena can certainly go through phase changes that move the entire system to a new plateau. Again, climate might be considered here but so too things like football—Kansas State University will likely never again consistently be among the worst programs in all of top-level college football.

Real estate might be examined under this cyclical framework. Perhaps the conventional wisdom that real estate is an above average investment (superior risk-adjusted returns) is false in that any apparent advantage was an illusion or temporary string of luck.

This is NOT going to be a thorough analysis by any means. Rather I am just passing along food for thought about what real estate might look like going forward compared to where it has recently been. At the same time it gives me a chance to introduce this concept of a cyclical perspective framework.

Here are three considerations I offer that imply a future somewhat different for real estate than the long-running path we have been experiencing.

More from less . . . peak land

YIMBY slowly defeats NIMBY . . . build, baby, build

The end of the bond bull market

Let’s take each in turn.

More from Less

One of the terrific features of a capitalistic free market is the strong incentives to continually reduce waste. Andrew McAfee illustrated as much in his book by the same title as this section, More from Less. The cumulative weight of all we consume is remarkably going down even as the amount we consume is worth more and more.

As it relates directly to land, this process can be seen in the fact that we have likely passed peak agricultural land needs. Despite needing to feed more people, we are able to do so using less land. Thus land is freed up for other uses. The effect of this is to reduce the marginal price of a unit of land. If this were the only example of this in terms of land use, it would be impactful yet ambiguous—non-agricultural land uses might now have newly unlocked value that actually might actually cause price to increase. Regardless of this possibility it doesn’t stop at agricultural land use.

The median size of a U.S. single family home has been declining over the past decade (peak was actually in 2015) having been somewhat stable before that period. This is despite the fact that we have become wealthier over this time span—a wealth effect that one would expect pushes in the opposite direction toward larger homes all else equal. Of course all else isn’t equal. We increasingly live in a world that encourages urban/suburban over suburban/rural. We also have more alternatives to satisfy our needs that substitute away from methods that require more space: food delivery reduces home kitchen needs, ridesharing reduces personal auto (garage) needs, innovations like flatscreen TVs reduce the amount of space used in a given room, etc. Thousands of small improvements each come with a lower need for space. Examined in isolation they may be trivial, but collectively they matter a lot.

Likely the biggest factor is smaller average household size as we are having fewer children on average. This perhaps dwarfs all the other forces combined for the time being—most of those are in their infancy (loose pun intended). Hopefully we reverse this trend and start having more kids. Additionally, I hope we start to welcome (many) more immigrants and continue to see wealth gains across all demographics. “But won’t that push up the demand for land?” I hear you ponder. Yes, that is where the next factor comes into play . . .

YIMBY slowly defeats NIMBY

The “slowly” part might be more accurately stated as slowly at first then faster and faster. This is my prediction at least. For those not acquainted, the acronyms are for Yes In My Back Yard and Not In My Back Yard. NIMBY is a fairly natural gut reaction people have to changes affecting their surroundings. They like it the way it is. However, this only becomes a problem when we loose track of a sound understanding of property rights.

You cannot literally put something in my backyard unless I agree to it. But I cannot rightfully stop you from putting something on your property unless I have a very good reason. A “very good reason” should mean something like a competing property right (e.g., like maybe the ability to see the Sun from my house); a legal easement (e.g., like maybe we entered into agreement that my sewer line would go under your yard); or a common law framework for nuisance (e.g., like maybe you cannot bring a smelly factory next to my family home). Without getting too deeply into the nuances of the issue, suffice it to say we have allowed the NIMBY veto to go from a very high threshold where it takes a lot for a NIMBY attitude to have any authority to a very submissive stance where NIMBY seems to be the default presumption.

As bad as it has gotten, I believe the tide is turning. YIMBY is predominantly more and more a policy stance favored by progressives while conservatives look to be abandoning a presumption of property rights in favor of a politically expedient NIMBY position. This is a positive development for YIMBY for the following reasons:

Conservatives are almost always on the losing side of a change in policy. Conservative positions are by their nature a resistance to change. Success for conservatives is slowing change rather than offering change. Therefore, it is good to not have them as the agent for change.

Although politically expedient, the conservative adoption of NIMBY points of view is really nothing too new. After all, conservativism is about not changing. And NIMBY contrasts harshly with a fundamental conservative attribute in support of private property. So the conservative finds himself quite conflicted on the matter, which implies tepid support at best.

On the other hand progressives are generally successful at effecting change but bad at protecting the status quo. Having progressives embrace YIMBY gives it the better chance to carry the day in marginal battles than if conservatives were leading this crusade.

Elite experts are more and more adopting a YIMBY framework. To the extent progressives tend to be in power and tend to dominate policy, this is a favorable development.

What are the implications for real estate? NIMBY drives property values higher as it restricts supply. YIMBY unleashes supply in all its many varieties—truly letting 100 flowers bloom. Bryan Caplan’s upcoming book Build, Baby, Build will spell it out in much better illustration. In the meantime there is another factor at work . . .

The End of the Bond Bull Market

Real estate valuation can be summarized simply by the formula

Current Value = Net Operating Income / Capitalization Rate

In shorthand: Price = NOI / Cap Rate

The capitalization rate is the implied (required) return on investment in a fair market. For example if NOI is $100,000 and the cap rate is 5% then the price of the property should be $2,000,000 ($100,000/.05).

What goes into the cap rate? Well, current interest rates are a direct factor along with other factors specific to the property in question like a risk premium, liquidity premium, etc. Interest rates are fundamental as they represent the alternative uses of funds—what you could earn by investing elsewhere. And notice the relationship they have in the formula. As the interest rate increases it will increase the cap rate, which in turn decreases the value of the real estate.

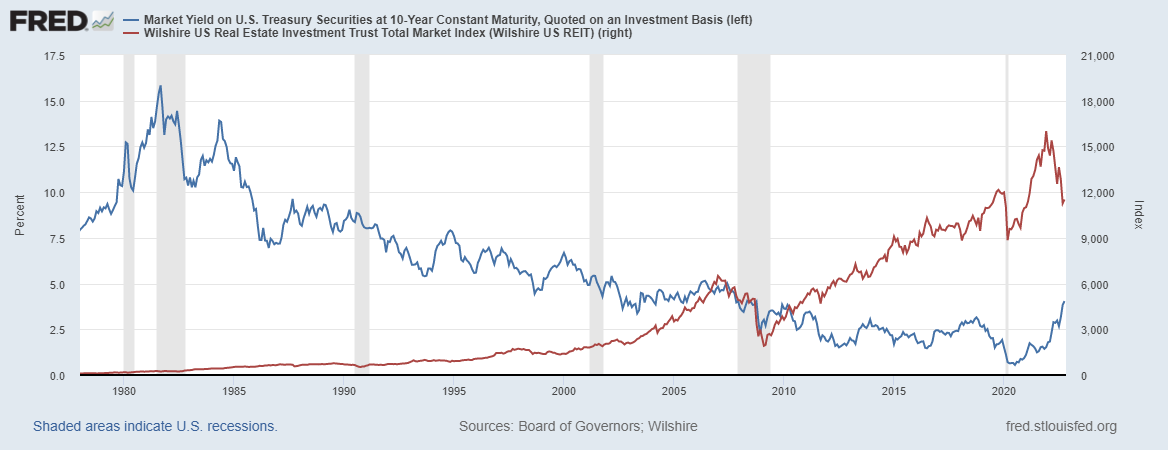

This makes sense, as your alternative rates of return go up, your willingness to pay for the property goes down. Price is inverse to interest rates. Well, what has been the general trend for the past 45 years with interest rates in the U.S.? Recent events notwithstanding, rates have been in a steady decline—the so-called bond bull market (bond prices going up as rates go down). Here is a graph of the 10-year U.S. Treasury rate plotted suggestively against the Wilshire U.S. REIT Total Market Index:

I say “suggestively” since there are obviously other factors at play that affect both of these variables, and the 10-year UST is not the only interest rate to be considered. But we know from the straightforward math and economic reasoning that interest rates declining will unambiguously increase the value of real estate, ceteris paribus.

While rates have recently increased quite a bit very quickly in response to inflation, they have not increased substantially enough to allow for a decline like what was experienced from 1980-2021. This end of the interest rate bear market (bond bull market) has to be at least the removal of support for, if not a headwind to, real estate valuation going forward.

I may be overstating any or all three factors, and there may be other factors that dominate these even if I have each appropriately gauged. Regardless these are strong considerations to keep in mind as we make educated guesses about what the future of real estate investment looks like.