A year ago in this post I made the following observations (please forgive me the extend excerpt):

Large stocks in the U.S. are most likely greatly overvalued. Those investing in them might very well be in for a rough ride one way or another.

I say “most likely” because, hey, who knows? Maybe the extraordinary future that is currently being priced into just those securities—they are basically, interestingly alone in this position—portends a magnificent future just for them. Or maybe, hear me out, maybe valuation still matters.

. . .

Let’s focus on all large U.S. stocks (growth and value) using the more familiar S&P 500 Index. For it we can calculate the same P/S ratio.

As pointed out in the chart above, the price (valuation) at which you buy stocks ends up mattering quite a bit. Over longer periods of time like +10 years stock returns inversely correspond to valuation multiples. Valuation is a poor timing tool (perhaps a subject for a future post), but it is a great predictor of long-term returns.

The signal it is giving us is a very clear warning sign. We should strongly consider finding alternatives away from large U.S. stocks.

. . .

So perhaps small (especially value) rather than large stocks in the U.S. should attract investor attention and international4 (especially value again) rather than U.S. should as well.

. . .

So, back to the implied question posed in the title of the post: Where am I putting my money?

While maintaining diversification across the broad landscape of stocks and bonds, I am following these guidelines:

Minimizing exposure to large U.S. stocks especially large growth

Maximizing exposure to value stocks in U.S. small cap, developed markets, and emerging markets

Increasing my exposure to investment-grade bonds although this remains fairly small for me

The bulk of my investment portfolio can be found in the red and blue circles below where red is a considerable amount of my concentration.5

FWIW, that is where I’m putting my money.

I noted in the piece that valuation, while critically important for long-term investment expectations, was a poor timing tool . . . but . . .

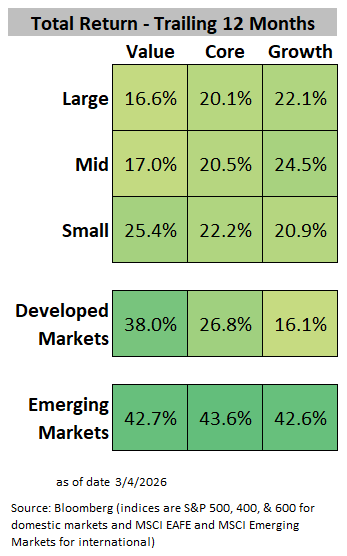

The past year has been very kind to this allocation. Here are the 12-month returns through March 4, 2026 overlaid in the same style-boxes:

Yes, everything is up. However, small cap value is the best performer among the U.S. stock groups and international value is stealing the show with emerging markets really shining.

It’s just been one year, so let’s not get ahead of ourselves, but at least the recent relative changes make sense from the standpoint of my original hypothesis.

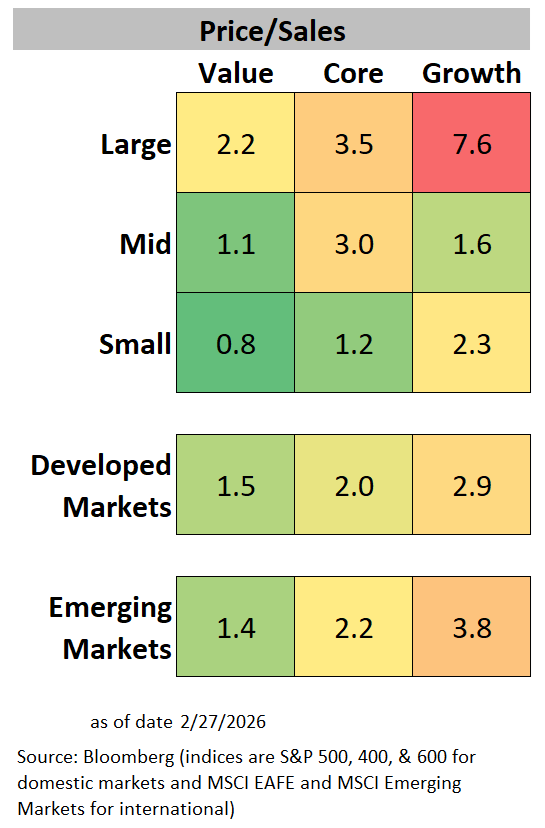

Checking in on the two main valuation metrics I examined previously, price to sales and price to (long-term, inflation adjusted) earnings, we see that the problems/opportunities I was identifying really are still in place. If anything, large U.S. stocks look EVEN WORSE. And small value stocks look even better despite having outperformed their large counterparts in the U.S.

Here is the price to sales grid updated through the end of February:

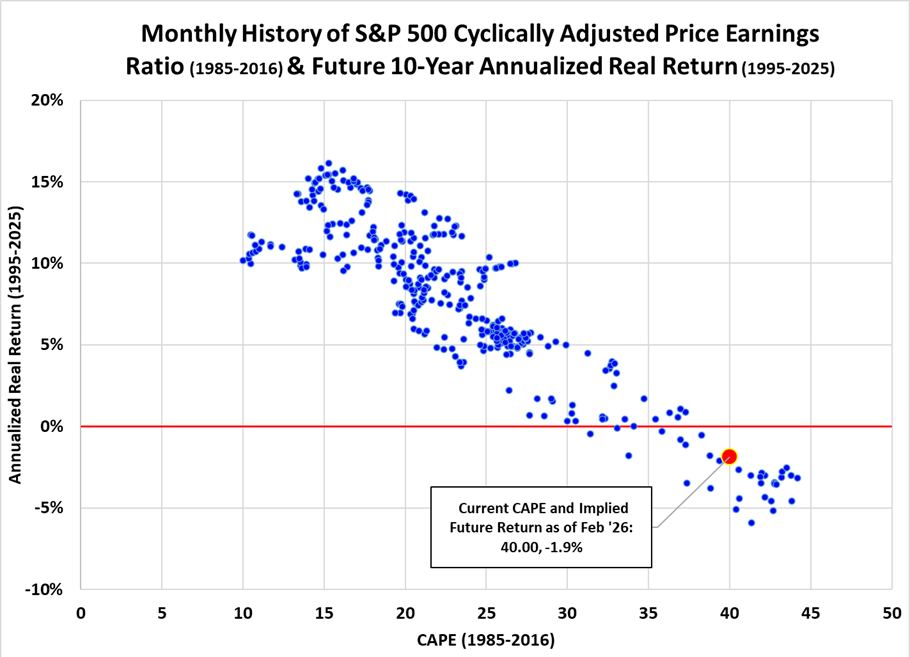

And here is the CAPE (you’ll have to click back to the prior piece to compare):

Source: Bloomberg & Multpl.com

Don’t lose the Redwood tree for the forest. The chart is showing future implied real returns (adjusted for inflation) for S&P 500 stocks to be negative. Specifically, -1.9% per year on average or -17.5% for a decade in total.

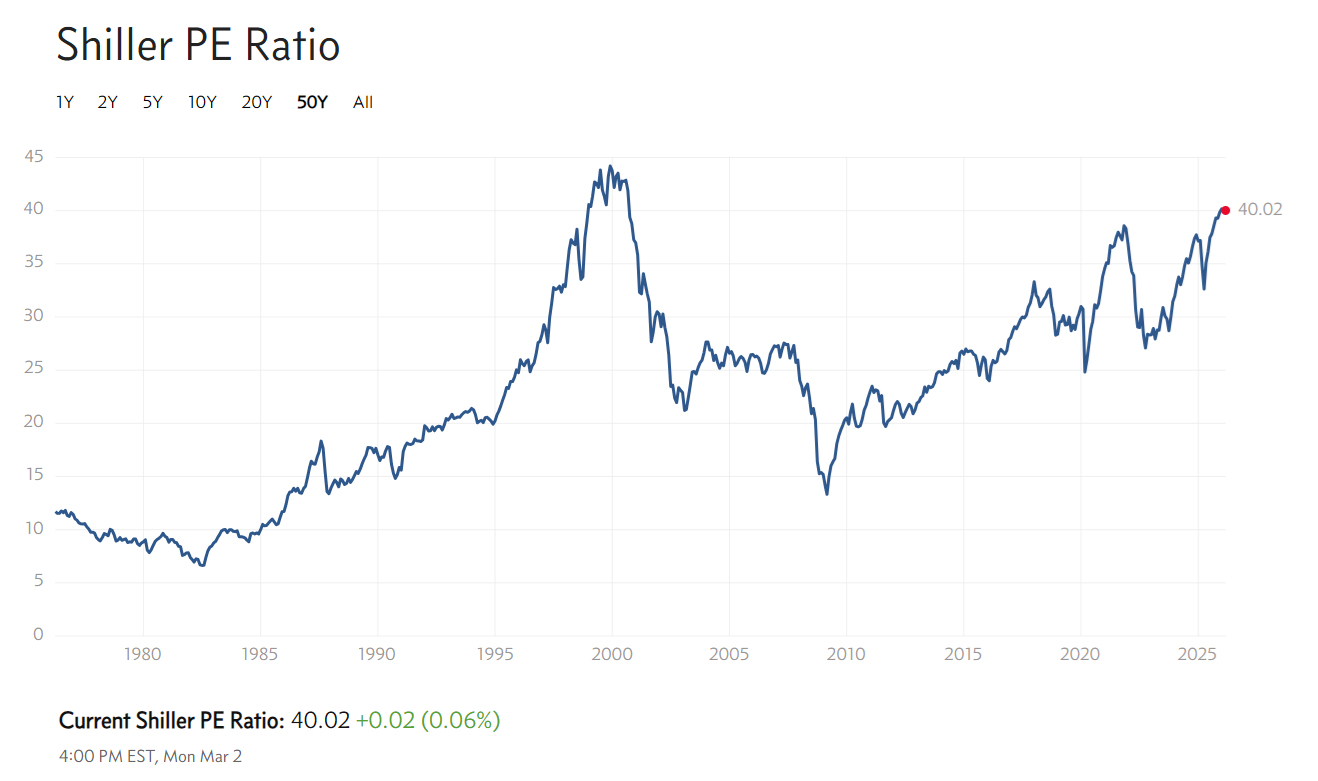

Another way to view the valuation history of CAPE is to chart it directly as done here from Multpl.com (all-time history followed by just the last 50 years):

Source: Multpl.com

Source: Multipl.com

Note that the current figure at 40.02 is about 50% higher than it was just before the Great Recession and closing in on how high it got in the Dot Com era. This is not a good outlook for U.S. large stocks simply because using either history or theory as our guide tells us that the future expected returns from them just can’t be that good.

This raises the question: How am I invested today? The answer for me personally is not too different at all. I still very much favor small value companies in the U.S. as well as value companies throughout the rest of the world (developed and emerging markets).

Sure, the current thing™, war in Iran, has been a headwind for international stocks in particular and somewhat stocks in general with small companies suffering a little more than large. None of that does much to deter my long-term view, which is grounded in valuation and a strong belief that the future will be a lot like the past in the long run. That is to say, I am a long-term optimist (economically and as an investor) in spite of being short-term pessimistic about all kinds of things.

In no likely world to come (good or bad) does valuation not matter. And valuation is screaming at us to pay attention to the generational opportunities and risks before us now.

Magnitude Matters is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

This is not intended and should not be construed as investment advice.